|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||

|

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Selling in 2027 doesn’t mean waiting until 2027 to act. The most confident downsizers use the years leading up to their sale to make thoughtful, low-stress decisions.

Focus on flexibility, not rigid timelines

Instead of locking yourself into a date, focus on understanding:

Flexibility gives you control when opportunity appears.

Reduce future friction, one step at a time

Small steps now make a big difference later:

This protects your energy — not just your finances.

Storage deserves its own strategy

One of the most common regrets I hear from downsizers is:

“I didn’t realize how much I’d miss having easy access to my things.”

Before you move:

Whether it’s bikes, skis, kayaks, or travel gear, convenient storage often determines long-term satisfaction.

Remember: downsizing is a process

The goal isn’t just to sell a house. It’s to move into a home that feels lighter, easier, and aligned with how you want to live next.

Items of Note for January

A Promising Start to the Year in the North Okanagan

2026 is off to a solid start here in the North Okanagan! While many parts of BC saw slower sales in January, our market held remarkably steady. Home sales were down just 1% from last year and sit about 10% below the 10-year average — much stronger than the provincial picture, where sales dropped more than 24% and 31% respectively.

Prices remained fairly steady. The median sale price rose 8% year-over-year to $680,000, the average price came in at $685,756 - up 3%, while the overall composite benchmark price eased slightly.

With interest rates holding steady, the North Okanagan continues to show resilience and stability. All in all, a fairly solid kickoff to the year!

Sales

North Okanagan Unit Sales were down 1% Year-over-Year (79 vs 80) and come in 10% below the 10 Year Average.

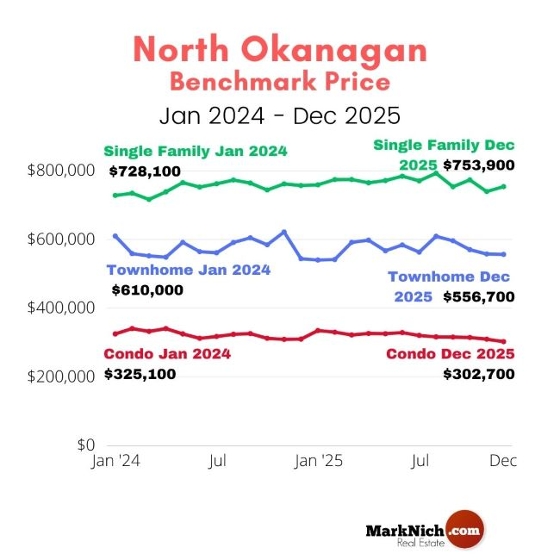

Benchmark Price

Composite Benchmark Selling Price for the North Okanagan since March 2020.

New Listings hitting the market were down 15% Year-over-Year (176 vs 207) which is about 7% above the 10-Year average (165).

Active Listings are unchanged Year-over-Year (676 vs 677), which puts the North Okanagan about 14% above the 10 year average (593) for the month of January.

The overall North Okanagan market downgraded from a balanced market to straddling the fence between a Balanced Market and a Buyer's Market.

The Sales to Active Listings ratio is 11.6% (down from 14% in Dec).

Between 12-25% is considered a Balanced Market.

The Sales to New Listing ratio is 45% (down from 86% in Dec).

Between 40-60% is considered a Balanced Market but ratios skew higher in the winter months when the number of new listings hitting the market are low.

Days to Sell Average is 83 days. This is up slightly Year-over-Year (82) and up from December (81).

Unit Sales in the Central Okanagan for January were down 16% Year-over-Year (203 vs 241), which is 21% below the 10 Year Average of 257.

Benchmark Price

December saw 767 New Listings hit the market, which is down 13% Year-over-Year (885) and 26% above the 10-Year Average of 607.

And the 2323 current Active Listings is down 4% Year-over-Year (2414) and is 38% above the 10-year average of 1689.

With a Sales to Active Listings ratio of 9% and Sales to New Listings ratio of 26% the Central Okanagan continues to be in a Buyer's Market.

For the full report click here

Selling in 2027: Why Downsizers in the North Okanagan Benefit From Thinking Ahead

If your goal is to sell in 2027, you’re already ahead of the curve just by thinking about it now.

The smoothest, least stressful sales are rarely rushed. They’re planned.

Market cycles matter — especially locally

The Vernon and North Okanagan market shifts with interest rates, inventory levels, and buyer demand. Planning ahead allows you to:

When you’re informed early, you get to choose when to act — not feel forced.

Equity planning is central for downsizers

For many homeowners, the family home represents decades of equity. Early planning helps you:

Clarity reduces anxiety and makes the next step feel achievable.

Storage and lifestyle planning belong here too

Many people don’t think about storage until after they’ve sold — and that’s often when regret sets in.

Ask yourself now:

These questions shape better decisions — long before you list.

Think about future you

Health, energy, and mobility change. Planning early lets you:

Downsizing in 2026: How to Prepare Your Home Without Overdoing It

If 2026 is your target year to downsize, preparation is your biggest advantage. What you do before you list often has a greater impact on your outcome than what you do once the sign goes up.

The biggest mistake downsizers make? Waiting too long to prepare — then feeling rushed.

Declutter early, but with intention

Start where buyers won’t see — and where stress quietly builds:

This isn’t about purging everything. It’s about identifying what truly needs to come with you — especially items tied to your lifestyle.

Decide what’s worth keeping close

This is the moment to separate:

If you ski every winter, bike weekly, or paddle all summer, you’ll want a future home that accommodates that without friction. If you travel all winter, your storage needs will look very different.

Downsizing works best when your next home supports your life — not when it forces constant compromises.

Focus on updates that buyers actually value

You don’t need a full renovation. In Vernon’s established neighbourhoods, buyers respond best to:

Homes that feel clean, bright, and well cared for consistently outperform those that feel dated or deferred.

Get a planning conversation early

A no-pressure review 12–18 months out helps you:

Preparation creates options — and options create leverage.

If you’re considering downsizing in 2026, the most important work doesn’t start with listings, floor plans, or even price ranges. It starts with understanding why you want to downsize — and how you actually live day to day in the Vernon and the North Okanagan area.

Downsizing done well isn’t about giving things up. It’s about right-sizing your home to fit your next chapter.

Local downsizers often share similar goals, but they don’t all need the same type of home. Ask yourself:

Your answers shape every decision that follows — especially what type of home will work best.

Many people focus on “smaller,” but the real shift is toward simpler living. In the Okanagan, that often means prioritizing:

A 1,400 sq ft home that’s well designed can feel far more livable than a poorly laid-out 2,000 sq ft house.

This is where many downsizing plans quietly fall apart.

Before choosing your next home, take an honest look at what you actually use and enjoy:

Many downsizers quickly realize that off-site storage units are inconvenient, costly, and frustrating over time. Repeated trips across town to grab gear often take the joy out of the lifestyle they were trying to preserve.

In this market, smart downsizers look for:

Downsizing is both practical and emotional. Starting early in 2026 gives you time to:

The goal isn’t to move fast — it’s to move well.

When many new Canadian homebuyers calculate whether they can afford a new home, they focus almost exclusively on one number: the monthly mortgage payment. It’s the figure lenders use for the mortgage stress test, the number real estate agents discuss during showings, and the benchmark buyers use to determine their budget.[ratehub]

However, the mortgage is only the starting line. Homeowners also pay for property taxes, insurance, utilities, strata special levies, surprise repairs, and ongoing maintenance. According to housing cost breakdowns from Ratehub, these non-mortgage expenses can easily add $1,500 or more per month on top of the mortgage, depending on the home and location. When you factor in these costs, a $3,000 monthly mortgage can quickly push total housing expenses well beyond $4,500 per month.[ratehub]

So while qualifying for a mortgage answers one question, “Can a bank trust you with this loan?”, it doesn’t answer the more important one: “Can you comfortably maintain this lifestyle?”

In today’s market, about one in four Canadian homebuyers report experiencing at least some post-purchase regret. While most homeowners remain satisfied, research shows that regret often emerges when the true cost of ownership—such as maintenance, repairs, and ongoing living expenses—was higher than expected. To reduce the risk of buyer’s remorse, it’s critical for homebuyers to plan not just for the mortgage payment, but for the full cost of living in the home.ratehub+1

Property Taxes

Property tax bills have been rising in many Canadian cities as municipalities work to fund infrastructure and services. In 2024, the median year-over-year change in property tax rates among 24 major Canadian cities was about 4.9 percent, with some regions experiencing even greater increases.[zoocasa]

Property taxes aren’t fixed. Reassessments and rate changes happen regularly, and as neighbourhood values rise, so do tax bills even when the rate stays the same.[zoocasa]

Home Insurance

As of 2026, home insurance premiums in Canada have entered a “new normal.” Record weather-related losses in recent years, combined with higher rebuilding and replacement costs, continue to push insurers to raise rates and reassess risk across many regions.[ca.investing]

In some provinces, home insurance premiums have increased sharply over the past decade, with upward pressure emerging nationwide. As insurers recalibrate risk at the postal-code level, homeowners can see their premiums rise $100–$200 per month in a single year—even without making a claim or changing coverage.[ca.investing]

Condo and Strata Fees

For buyers entering the condo market, monthly fees typically range from $0.60 to $1.00 per square foot, depending on the building and amenities. These fees are mandatory and are used to fund day-to-day operations as well as long-term reserve funds for major repairs.[ratehub]

By contributing regularly, owners help reduce the risk of large, unexpected special assessments later on.[ratehub]

Utilities

Homeowners should budget between $250 to $600 monthly for utilities including electricity, heating, water, internet, and phone services, with costs varying based on your home’s size and location. These expenses often come as a surprise to first-time buyers, particularly those transitioning from apartment living where some utilities may have been included in rent. Larger homes naturally require more energy for heating and cooling, while properties with outdoor spaces may see higher water usage during warmer months.[ratehub]

The "Commuter Tax"

There’s also what might be called “the commuter tax.” Moving to suburban markets for a cheaper house can increase gas and transit costs that often negate the mortgage savings. That apparent price difference can disappear quickly if you’re spending hundreds of dollars more each month on commuting.

Routine Maintenance

Beyond emergencies, Canadian homes require ongoing care: lawn service, gutter cleaning, pest control, HVAC servicing, snow removal, and seasonal tasks. These aren’t luxuries for many households—they’re practical solutions to time constraints and property upkeep in Canada’s demanding climate. Collectively, these services can add $200–$400 monthly to ownership costs.[ratehub]

Major System Replacements

This is where many Canadian homeowners get caught off guard. Maintenance and repairs aren’t a matter of if but when—and rising labour and material costs have made these repairs significantly more expensive in recent years.[ca.investing]

According to Statistics Canada and industry cost reports, home repair and maintenance costs have increased materially since 2018, driven by construction inflation and labour shortages. As a result, homeowners are commonly advised to budget 1%–2% of their home’s value annually for maintenance and long-term repairs.ratehub+1

Major system replacements can add up quickly:

Roof replacement: $8,000–$15,000+

HVAC (furnace or heat pump): $5,000–$12,000

Water heater: $1,200–$2,500

Foundation repairs: $4,000–$15,000+

These aren’t hypothetical expenses—they’re inevitable over time, with uncertain timing and rising costs.

Use the inspection as a planning tool. A 15-year-old furnace or aging roof signals $8,000–$15,000 in likely expenses within the first few years. That’s not a deal-breaker—it’s a budget roadmap. Buyers who understand these timelines can plan strategically instead of scrambling when systems fail.

Canada’s climate makes this worse. The “freeze-thaw” cycle wears down roofs, driveways, and foundations faster than in many milder climates, shortening the effective lifespan of key components. A roof that might last 25 years in a gentler environment may need replacement years sooner in parts of Canada.

Newer isn’t maintenance-free. Newer builds offer a temporary reprieve, but systems still age, warranties expire, and eventually every home requires major capital improvements.

Emergency repairs happen at the worst times. An HVAC failure during a cold snap, a burst pipe in winter, or ice dam damage to the roof—these scenarios happen when it’s least convenient and most expensive. Without liquid reserves, a single emergency can derail finances entirely.

Here’s what surprises many first-time Canadian buyers: the so-called “fixed costs” of homeownership aren’t actually fixed.

While a locked-rate mortgage provides payment stability for your term (typically 5 years in Canada), the other components—taxes, insurance, and condo fees—can climb significantly year over year due to inflation, climate risk, and local policy changes. A mortgage payment that felt comfortable at closing can feel tight three years later, even without lifestyle changes.[zoocasa]

The “2026 Renewal Wall” presents a significant challenge for Canadian homeowners. Approximately 60% of all outstanding mortgages in Canada are expected to renew in 2025 or 2026, with many owners facing substantial payment increases. Unexpected costs go beyond just maintenance and repairs. Many homeowners will experience sticker shock when their mortgage payments reset at higher rates upon renewal.collectorhq+1

The same gradual creep affects utilities, maintenance services, and every other aspect of homeownership.[ratehub]

Create a Dedicated House Repair Fund

Separate from emergency savings, this fund exists solely for home maintenance and repairs. Treat it like a non-negotiable monthly bill—set up automatic transfers so it happens without thinking about it.

The old rule of saving 1% of your home’s value annually for repairs is proving insufficient for some homeowners, particularly those with older properties or homes experiencing extreme weather. Aim for 2% if possible. For a newer home with recent updates, less might suffice. For an older property or one with systems nearing end-of-life, you’ll likely need to plan for greater costs.[ratehub]

Don’t Drain Your Savings at Closing

Cash reserves protect against surprises and prevent forced debt when repairs arise. If possible, keep a liquid emergency repair fund after closing rather than putting every available dollar into the down payment or immediate renovations. That breathing room matters more than most buyers realize.[ratehub]

Invest in Preventative Maintenance

Annual furnace servicing, gutter cleaning, and seasonal inspections catch small problems before they become expensive emergencies. A modest service call that prevents a major system failure is almost always worthwhile.

Create a seasonal maintenance calendar: HVAC checkups in spring and fall, gutter cleaning before winter, roof inspections after major storms. Consistency prevents costly surprises.

Leverage Canadian Tax Advantages

Consider leveraging Canadian tax advantages to build these reserves. First-time buyers should keep their FHSA (First Home Savings Account) open after purchase, or use the tax refund generated by it to seed their repair fund. The tax benefits you received while saving for the down payment can continue working for you as a homeowner.[ratehub]

Know Your Home’s Systems and Timelines

Understanding when major systems were last replaced helps predict future expenses. A 15-year-old water heater isn’t an emergency today, but it signals a likely expense within the first few years of ownership. Planning beats scrambling.

Long-Term Equity Building

Mortgage payments build equity with every payment. Unlike rent, ownership creates a forced savings mechanism that compounds over decades. In most markets, homes appreciate over time, multiplying the wealth-building effect.[ratehub]

Stability and Control

Homeowners control their living environment. Want to renovate the kitchen, paint the walls, landscape the yard, or install solar panels? Ownership provides autonomy that renting does not. That control has both lifestyle and financial value.[ratehub]

Predictability vs. Rent Volatility

While ownership costs rise gradually over time, rent increases can be sudden and dramatic. A fixed-rate mortgage provides a level of predictability that the rental market cannot match.ratehub+1

Yes, taxes and insurance increase, but the principal and interest portion—typically a majority of the total payment—remains locked for your term. Renters face volatility on 100% of their housing costs.ratehub+1

Lifestyle Benefits

Beyond finances, homeownership offers intangible benefits: deeper community roots, stability for families, space for hobbies, and the pride of building something that’s truly yours. These benefits have real value, even if they don’t appear on a balance sheet.

The key is ensuring the financial foundation supports the lifestyle, not undermines it.

The true measure of affordability isn’t what a lender will approve—it’s what allows you to sleep well at night when the furnace fails or your mortgage comes up for renewal.

The smartest buyers calculate affordability as “mortgage plus carrying costs” from the start. This might narrow the price range slightly, but it creates breathing room and peace of mind that makes a house feel like a home.[ratehub]

Homeownership remains one of the most powerful wealth-building tools available to Canadian families, but only when approached with financial realism rather than maximum leverage. Having an honest conversation about what affordability truly looks like isn’t about limiting dreams—it’s about making sure those dreams don’t become financial nightmares.[ratehub]

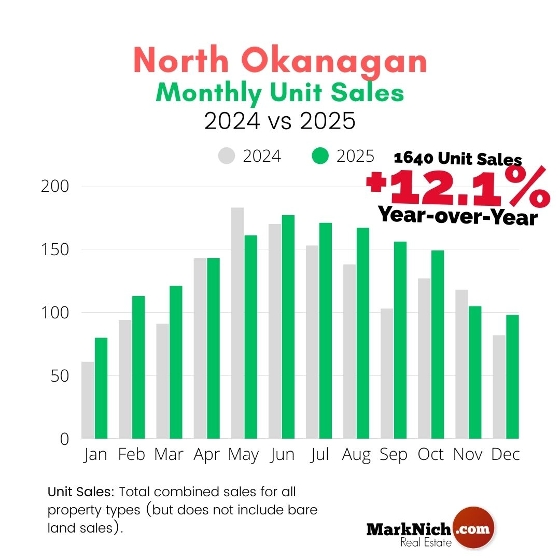

After a fairly strong start early in the year, the North Okanagan real estate market faced a few bumps before regaining some momentum to close 2025 on solid footing. Activity early on reflected confidence, but external factors — including market uncertainty tied to U.S. policies under President Trump and the impact of tariffs — briefly slowed things down through spring. By mid-year, however, the market regained some positive momentum, finishing in a balanced position with sales improving across the board.

The year began with notable strength. In January, sales soared 34% year over year, though they remained about 10% below the 10-year average. February continued the upward trend, up 20% over the previous year and tracking just 7% below the 10-year-average. Both months reflected absorption rates straddling between a buyer’s and balanced market.

March maintained solid year-over-year gains (+33%) but lost considerable footing versus long term sales figures coming in 28% under the 10-year average. By April, growth stalled, with no change over the previous year and continued weakness compared to longer-term trends. May marked possibly the lowest point of the year, with sales down 12% year over year and 21% below the 10-year-average; although the market did move back into balanced market territory.

The turnaround began in June, as confidence crept back into the market. Sales grew modestly by 4% compared to 2024 and closed 16.5% under the 10-year average — a marked improvement from spring’s gaps. July and August kept the momentum going with year-over-year increases of 12% and 21% respectively.

The fall months brought even stronger performance. September led the pack with a 51% year-over-year surge, bringing sales within 3.7% of the 10-year average. Things then cooled off for a couple months with October seeing an 18% bump year-over-year and 13% off the 10 year average, while November saw -10% and -20% respectively. December wrapped the year on a bright note with sales up 20% over 2024 and right on par with the 10-year-average average.

The Bank of Canada’s overnight rate started the year at 3.25% with 0.25% drops in January and again in March bringing the BoC rate down to 2.75% where it stayed until September. Rates came down 0.25% in Sept and again in October bringing the BoC rate down to 2.25% where it finished off the year

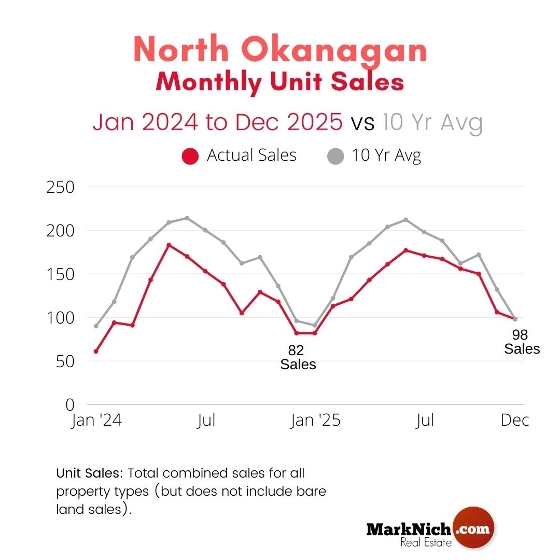

Despite spring headwinds, the North Okanagan market demonstrated resilience. Sales numbers versus the 10-year-average made fairly steady gains after March lows (-28%) and ended the year with sales equaling the 10-year-average in December (a first since March 2022).

Buyers benefited from interest rate relief and growing inventory through the year, while sellers saw balanced market conditions nine out of 12 months and renewed optimism as sales strengthened through the second half of the year (for the most part).

It may have been a bit of a finicky market for sellers, but with the right pricing strategy homes sold (and often sold quickly).

Compared to many markets around the province - especially Greater Vancouver and the Fraser Valley - the North Okanagan faired quite well.

With slowly growing demand, good inventory levels, and with interest rates predicted to remain steady through 2026 the North Okanagan real estate market looks poised to continue to slowly gain strength. While not a hot real estate year by any means 2025 did show continued growth and ended with stronger sales numbers than 2024 and 2023.

Items of Note for December

Sales

North Okanagan Unit Sales were up 20% Year-over-Year (98 vs 82) which equals the 10 Year Average of 98. After being close to beating the 10 Year Average in September sales slowed down in Oct and Nov but December ended the year on a strong note. Not only was it the first time since April 2022 that sales didn't come in below the 10 Year Average but it was also the strongest December in four years.

Benchmark Price

Composite Benchmark Selling Price for the North Okanagan since March 2020.

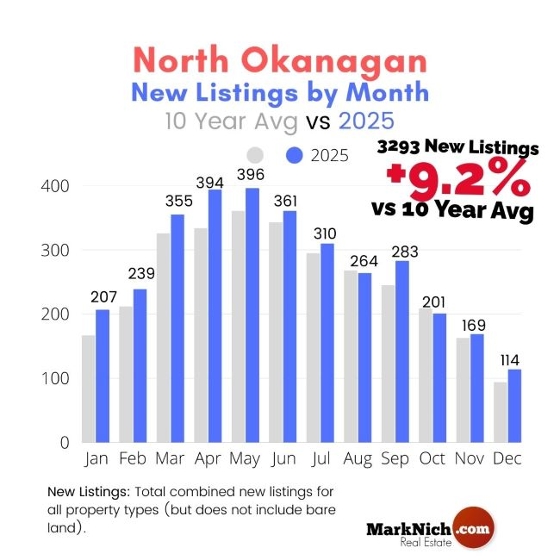

New Listings hitting the market were up 13% Year-over-Year (114 vs 101) which is about 21% above the 10-Year average (94).

Active Listings are up 12% Year-over-Year (710 vs 634), which puts the North Okanagan about 20% above the 10 year average (594) for the month of December.

The overall North Okanagan market continues to be in a balanced market.

The Sales to Active Listings ratio is 14% (up from 13% in November).

Between 12-25% is considered a Balanced Market.

The Sales to New Listing ratio is 86% (up from 63% in November).

Between 40-60% is considered a Balanced Market but ratios skew higher in the winter months when the number of new listings hitting the market are low.

Days to Sell Average is 81 days. This is down Year-over-Year (99) and unchanged from November (81).

Unit Sales in the Central Okanagan for December were down 4% Year-over-Year (240 vs 250), which is 13% below the 10 Year Average of 277. If you recall, November sales came in 25% below the 10 Year Average.

Benchmark Price

December saw 365 New Listings hit the market, which is up 9% Year-over-Year (334) and 13% above the 10-Year Average of 324.

And the 2358 current Active Listings is up 2% Year-over-Year (2309) and is 42% above the 10-year average of 1665.

With a Sales to Active Listings ratio of 10% and Sales to New Listings ratio of 66% the Central Okanagan continues to be in a Buyer's Market.